Behind Europe's banking crisis

Dick Nichols responds to a comment by Jurriaan Bendien on his

November 1 article " European financial system: next crash just around the corner?"

December 2, 2016 — Links International Journal of Socialist Renewal — Thanks to Jurriaan Bendien for his comment, and my apologies for not finishing this reply earlier. A lot has been happening in the Spanish state that needs covering and it also took me quite a bit of research to work out what I make of the issues Jurriaan raised.

To begin, I agree that it was misleading to write that “the chief pressure squeezing bank profitability has come directly from the real economic conditions, from the subdued demand for loans” (emphasis added here). Real economic forces such as the level of consumer demand don’t operate directly on the banking sector as they do on firms producing commodities for sale on the market, but indirectly, mainly through changes in interest rates.

However, I still hold to the point I was trying to make with that wrongly worded sentence. That is, of the forces shaping bank profitability it is the subdued demand for credit that is most driving actual levels of lending to business and, as a consequence, also compressing banking sector profitability in Europe.

The subdued demand for credit is in turn the result, primarily, of the low rate of private business investment combined with the availability — for big business — of other sources of funds (chiefly its own retained profits, which have climbed from 12% to 22% of GDP since 2000). According to the latest Economic Bulletin (November, 7/2016) of the European Central Bank (ECB), “the decline in the growth rate of fixed capital formation has led to a deceleration in the growth of Euro Area capital since 2008 which is unprecedented in a historical perspective.”

In this still-stagnant economic environment, laying the blame for meagre bank profits on low and negative interest rates is a bit like a small business person railing against the tax man when fewer and fewer customers are coming through the door.

Credit demand and supply

For banks, the amount of credit (loans) they can supply is determined by some mix of: funding costs, balance sheet restrictions (like capital, liquidity and leverage ratios and percentage of non-performing loans that have to be allowed for), intensity of the competition they face and their appetite for risk. For enterprises, credit demand is shaped by some mix of: profit expectations and opportunities, risk appetite, interest rates on loans and the availability of alternative funding sources (like their retained profits and own bond issuance).

The forces determining movements in credit supply and demand as well as bank profitability change according to the phase of the business cycle. A dramatic example of an extreme supply-side constraint came with the late-2008 crisis after the Lehman Brothers collapse, when inter-bank credit all but dried up in an atmosphere of extreme distrust. Supply side constraints also reappeared in 2010, when the sovereign debt crisis in the European “periphery” emerged.

However, I was focussed primarily on the whole post-crisis period (first quarter of 2009 to today) with particular attention to the latest period of the weak recovery (mid-2013 to today). Bank profitability as measured by the return on equity, after crashing from highs of 20% in 2007 fell to below 5% in 2009 and has since then been more often than not under that number, even turning negative in early 2014 (see Figure 2 in article).

This state of affairs has prevailed despite the partial economic upturns of 2009-2011 and 2013-2016 and despite banks’ cost of equity — the return theoretically paid to shareholders to compensate for the risk they undertake investing their capital — having fallen by 2015 to just above pre-crisis levels (see Figure 2 below).

In recent years there’s been a lot of research (surveys of banks, econometric studies) on how much loans to business by European banks have been conditioned in the post-crisis period by constraints on banks’ capacity to lend and how much it is due to the level of credit demanded by business (and households, but my focus is on businesses). This discussion is important, not only because bank credit accounts for over 80% of debt financing to non-financial corporations in the Euro Area but also because it also raises the question of whether there aren’t better ways of financing the investments society needs.

Information on the relative impact of these demand- and supply-side factors are contained in the European Central Bank’s (ECB) quarterly Bank Lending Survey (BLS) of 140 Euro Area banks and its Survey of Access to Finance of Small and Medium Enterprises (SAFE). ECB Occasional Paper 179 (September 2016), The euro area bank lending survey, provides a useful summary of the results of the BLS since it began in the first quarter of 2003.

The data on credit to business — in the ECB series Monetary Financial Institutions (MFI) Credit to Non-Financial Corporations — gives detailed information about the levels of credit actually granted, both at the level of the Euro Area and of individual member states (see Figure 1 below).

Low and negative interest rates

A bank’s profitability depends basically on its loan book: the bulk of its profits usually comes from all the loans (to business, for housing and as consumer credit) that generate interest income. Clearly a major influence on both bank credit supply and demand is the level of interest rates. Central bank monetary policy aimed at stimulating or restraining growth and inflation operates through manipulation of the interest rate at which banks can borrow from or lend to it (the policy rate). This rate sets the floor for rates paid and charged on all classes of deposits and loans (the “interest rate structure”).

In normal conditions of positive interest rates the level of this policy (or base) rate shouldn’t affect bank profitability. If a bank is borrowing at 2% from the central bank it can lend to clients at 5%: if it is borrowing at 3.75% it can lend at 6.75%. In theory, therefore, its interest margin (here 3%) shouldn’t be affected by the prevailing level of rates.

However, it is up for questioning whether this argument holds if the policy rate is very low or even negative, as it presently is in the Euro Area, Japan, Sweden, Denmark and Switzerland. Are bank interest margins and profitability inevitably squeezed in such a situation? What is the impact on bank lending? Focussing on the present-day Euro Area, to what degree are these low and negative rates responsible for the subdued growth in bank lending to business and the decline in bank profitability there? I look at these three questions one by one.

Are bank margins inevitably squeezed in an environment of low and negative interest rates? What is the impact on bank profitability?

This question is addressed in an October 2015 Bank for International Settlements (BIS) Working Paper called “The influence of monetary policy on bank profitability” and in an April 2016 Federal Reserve Board International Finance Discussion Papers note called “’Low-for-long’ interest rates and net interest margins of banks in Advanced Foreign Economies”.

It is also the subject of an article in the April 2016 Monetary Policy Report of the Riksbank (Swedish central bank) entitled “How do low and negative interest rates affect banks’ profitability?”, which reads in part like an implicit criticism of the BIS paper.

The Riksbank article looks to explain the apparent contradiction between the low return on equity for Euro Area banks and the high return on equity (between 11% and 14%) for major Swedish banks even though both groups face a negative policy rate. It attributes the difference to the following factors:

• Banks will, by definition, experience a squeeze on their interest margin if they decide not to pass on to depositors the negative policy rate charged them by central banks (this is the case to date with the majority of banks facing a negative rate). However, this decision has a smaller impact on their profitability the less they rely for their funding upon deposits as opposed to borrowing on financial markets. Swedish banks source over half their funding from financial markets while the total loans they extend are over three times the deposits they hold. By contrast, Swiss banks lend only about 90% of the deposits they hold.

Since low or negative interest rates also lead to a fall in the cost of borrowing, the losses incurred by the decision not to charge depositors negative rates will be offset to some degree by cheaper borrowing rates. In Sweden, the end result is that the four big banks (Nordea, Swedbank, SEB and Handelsbanken) have funding costs among the lowest in Europe.

• With lower funding costs, banks can offer lower lending rates to existing customers, in turn increasing their capacity to meet loan repayments and reducing the percentage of non-performing loans on their books, again helping profitability.

• Lending volumes will increase as the demand for loans increases with lower rates, also boosting profitability. A reduced interest margin doesn’t necessarily mean reduced profitability if loan volume is expanding enough to offset the margin reduction.

• If low interest rates stimulate lending and investment, the demand for other bank services, such as for capital management and investment banking, may also increase, leading to increased fee income.

• The overall impact of banks’ having to pay the central bank for holding their surplus cash is very small compared to total bank assets.

The Riksbank study concludes that “there is nothing to suggest that low and negative rates have so far had a negative effect on banks’ profitability. The profitability problems among banks in the Euro Area can instead be explained by more fundamental problems with a large proportion of bad loans in combination with high costs.” (emphasis added)

However, this conclusion seems (to date) a minority view. The BIS study (of 109 large international banks) cites previous econometric studies that show a link between higher interest rates (especially longer term rates) and higher bank income. It itself finds that there is:

a positive relationship between interest rate structure and bank profitability [and that] the impact of interest rates on bank profitability is particularly large when they are low. All this suggests that, over time, unusually low interest rates and an unusually flat term structure [difference between short- and long-term interest rates] erode bank profitability.

The FED study, which found clear evidence that interest margins get compressed as interest rates approach zero, was more guarded in its conclusion as to the impact on bank profitability:

The impact of interest rate changes on overall bank profitability and capital adequacy positions is more ambiguous as it will vary on the state of the economy. For example, if low interest rate environments tend to happen in a period where demand for loans is low as well, or where banks are (capital or otherwise) constrained and otherwise deleveraging after a financial crisis, this may (further) suppress Net Interest Margins and overall profitability, especially when banks are also facing balance sheets problems and deleveraging, say in the wake of a crisis. The net impact on asset quality and non-performing loans, which feed into profitability, is more ambiguous as low rates make on one hand loan payments easier for borrowers but also may be associated with poorer quality borrowers getting loans. More generally, the state of the economy will importantly both influence the scope for profitable banking business and the level of interest rates.

The high profitability of the Swedish banks would then seem to be an exception to the rule. BIS Head of Research Hyun Song Shin addressed the possible causes at an April 7 ECB conference in Frankfurt, mentioning Swedish banks’ lesser dependence on customer deposits but in particular stressing a factor not touched on in the Riksbank article — their ability to exploit Swedish krona-euro currency swaps. Hyun Song Shin writes:

Swedish banks are sensitive to monetary developments in the Euro Area, and especially to the shape of the euro yield curve [tracing out the changing yield on bonds of different maturities]. In recent months, Swedish banks have taken advantage of low long-term borrowing rates in euros, and have been issuing euro-denominated bonds of longer maturity. The banks then swap the the euros for Swedish krona in the capital market, meaning that they borrow Swedish krona by pledging the borrowed euro funds as collateral. Having borrowed the Swedish krona, they lend it out to domestic borrowers in Sweden.

Australian and Norwegian banks carry out similar operations — borrowing in lower-interest currencies (like the yen) and then swapping these borrowed funds into the domestic currency for lending at a higher interest margin than would have been the case had they borrowed domestically. It is the position of Australia, Sweden and Norway as economies having growth and interest rates higher than those prevailing in Japan or the Euro Area that allow this funding tactic: it is not available to banks in the economies where lower growth and interest rates prevail.

The answer to Question 1 would seem to be that bank profitability is squeezed in a low interest rate environment, but not in every instance.

Do low and negative rates always lead to subdued growth in bank lending?

From this answer to Question 1 it would seem that Jurriaan is expressing the majority position of researchers when he argues that “banks have been ‘under pressure to curb their lending’ [and that] the ‘chief pressure’ is simply that interest rates are low.”

If this were universally true we would expect bank lending growth to be stagnating in all countries where low and negative interest rates prevail. But this is not the case, with Sweden again providing the counter-example.

Hyun Song Shin’s study compares growth in loans to non-financial firms and households in the economies with negative policy rates from the first quarter of 2014 (when the phase of negative rates began) to the first quarter of 2016. He notes “how diverse the experience with credit growth has been”.

Credit growth to firms and households turned positive in the Euro Area last year, and is running at around 1% per year while in Switzerland the growth rate has fallen from an annual rate of 8% at the end of 2014 [to -2% at the end of 2015]. But the case that stands out is Sweden, where lending has been growing at close to 6% annually. The contrast between Sweden and Switzerland is especially noteworthy.

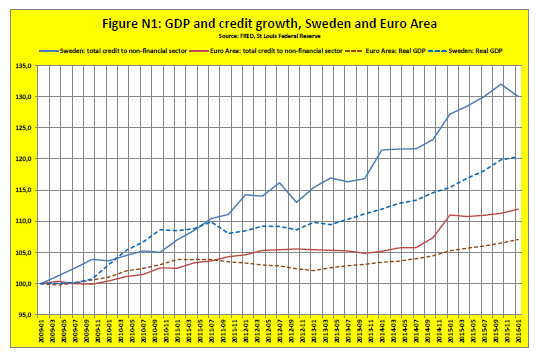

Figure 1

It is implausible that the supply-side factors producing lower funding costs alone explain these differences. Relying on finance markets (particularly in the Euro Area) means that Swedish banks are able to lend at rates lower than otherwise would be the case or maintain an interest margin that would otherwise be narrower.

These factors would provide only a slice of extra profit in addition to that generated by the high level of credit demand (see Figure 1). It is the high growth rate of the Swedish economy and not any special funding advantages for banks that is driving the high growth rate of credit to firms and households in Sweden. Annual Swedish GDP growth averaged 3.5% from the first quarter of 2014 until the second quarter of 2016 (as against 1.65% for the Euro Area).

Also, the most important component of Swedish growth was investment growth as measured by the average annual increase in gross fixed capital formation (Sweden 6.6%, Euro Area 2.5% over the same period, see Figure 2).

Figure 2

Unsurprisingly, over the entire period (2014Q1 to 2016Q2) bank credit from resident Swedish banks to households and non-financial firms increased by 11.3% as against 6.75% for the Euro Area (BIS figures).

The results for Denmark, Japan and Switzerland show the same sort of relationship over the same period: very sluggish annual average GDP growth of 0.95%, 0.34% and 1.44% respectively, accompanied by low bank credit growth to households and non-financial firms (respectively of 1.37%, 2.66% and 3.16%).

The answer to Question 2 would then be: “In general, the chief determinant of subdued growth in bank lending is low growth, not low interest rates.”

What about the Euro Area — are low and negative rates chiefly responsible for low credit growth there?

Jurriaan might object that he is not discussing this issue in general, but the actual situation for banks in the Euro Area today. He says, firstly, that here “at low interest rates, the bank profit margin on banks loans is rather small, and that it would take only a relatively small percentage of non-performing loans to ensure that the bank makes no money from the loan business at all.”

Is this accurate? With the exception of Greek banks that are still trying to recoup their past losses, it is certainly true that the net interest margin for European banks has been falling since April 2014, but this trend does not necessarily entail declining credit growth.

The BLS has had a semi-annual question on the ECB’s negative policy rate since April this year, and around 80% of reporting banks indicate that it has hurt their net interest income from all classes of loans, but with a small and increasing positive effect on lending volumes (which they also expect to increase).

That is, it is too soon to conclude that low and negative interest rates in the Euro Area will restrict bank credit availability. The outcome will depend, once again, on business expectations of growth and profits. (The latest data ECB Economic Bulletin speaks of “a moderate but steady recovery of the euro area economy” although “still subject to downside risks”.)

Jurriaan further notes that “most governments have imposed higher capital adequacy requirements and bank charge ceilings on banks, plus much stricter statutory loan qualifications on borrowers, which mostly have to do with the borrower’s ability to repay. For every credit operation, banks now have higher administration costs and more legal requirements as well.”

How much have lending conditions tightened and how much have they curbed credit availability? The BLS covers the balance sheet constraints listed here under its category of “credit standards”, defined as “the internal guidelines or loan approval criteria of a bank”. According to the ECB Occasional Paper The euro bank lending survey, “banks’ cost of funds and balance sheet constraints (referring to cost of capital, access to funding and the bank’s liquidity position) and banks’ risk tolerance mainly determine banks’ loan supply, i.e. their willingness and ability to provide a loan.”

Since April 2014 the BLS has included an annual question on whether banks view credit standards as having tightened or eased since two periods in the past--the first quarter of 2003 (beginning of the BLS) and the second quarter of 2010 (intensification of the sovereign debt crisis in the European Union “periphery”).

The overall result as of the April 2016 BLS was that, while a majority or large minority of banks still see themselves in a phase of tighter credit standards for all types of loans compared to 2003, these standards are felt to have undergone considerable easing since 2010, with over 60% of banks viewing them as looser or basically unchanged. The percentage of reporting banks who view credit standards on loans to business as having eased since 2010 increased from 13% to 30% between April 2014 and April 2016.

In the immediate term, the number of banks reporting to the BLS that credit standards on loans to non-financial corporations have been easing over the previous quarter has since mid-2013 exceeded those reporting that they have been tightening. The last time this happened was before the crisis, in the June quarter of 2007.

This data makes me quite sceptical about the narrative of subdued loan growth as basically determined today by restrictive supply-side factors, especially when the ECB low-interest regime and special asset purchase programs have underpinned what investment and growth there has been (also by making more funds available to small and medium business than would otherwise have been the case). This scepticism is reinforced by a look at trends in bank loan demand from enterprises. Jurriaan doubts that there is a subdued demand for loans, but Figure 3, from the BLS database, surely suggests otherwise.

Figure 3

In the two other economic expansion phases since the BLS began (2003-2007 and 2009-2011) business demand for credit rises sharply, and then continues to increase at a slower rate until collapsing again at the onset of the next crisis. However, for the 2013-2016 recovery, the initial sharp rise turns from the beginning of 2014 into a downward trend. This leads in the beginning of 2015 into a flattening of growth in bank credit to enterprises (see Figure 1).

Moreover, this shift has taken place at the same time as firms, as consulted in the European Commission Survey on access of finance to enterprises, report that “restrictions in bank loan supply have gradually receded and have led to improvements in the availability of bank financing (loans and overdrafts).” (ECB Economic Bulletin 7, November 2016).

The Economic Bulletin also notes that non-financial corporations in the Euro Area hold record high liquid assets (around €2.5 trillion, boosted by years of wage compression), meaning that they can often fund future investment out of this vast pool of retained profits, reducing their reliance on bank funding.

Of course, this BLS data refers to the Euro Area banking sector as a whole, with the results expressing the balance of answers received. Individual banks and banks in specific industry sectors or countries, especially where cost structures are relatively higher, will still experience the situation Jurriaan describes, chafing at what are experienced as the supply-side constraints of excessively narrow margins and over-exacting regulatory requirements.

Conclusion

Pity Europe’s poor banks — haven’t they been punished enough for their role in the Great Financial Crisis and ensuing stagnation? Forced to amalgamate, taken over by governments, restructured, downsized, fined billions for their pre-crisis misdemeanours, forced to take “haircuts” on their holdings of Greek government bonds, hit with harsh regulations on capital adequacy, leverage and liquidity, plagued by lawsuits, loathed by millions: if all that were not enough, for two years now they have had their margins and profitability squeezed by the negative interest rate policies of stony-hearted central bankers.

They are having to put up with a smaller slice of the surplus that capital extracts from labour than that to which they were accustomed.

In this context, it is possible, even probable, that higher cost banks with rubbery capitalisations and big portfolios of non-performing loans — like Deutsche Bank and Monte dei Paschi di Siena — will fail and be bailed out in some way or other by the taxpayer. Is the answer, as Jurriaan seems to imply, that their chances of survival should be increased by raising interest rates (and their interest margins) sooner rather than later?

Surely ECB president Mario Draghi is right when he says — answering the attack of politicians who have accused ECB low-interest rate policies of expropriating retirees’ savings — that without its “standard and non-standard” monetary policy measures providing trillions of euros of liquidity into the economy “unemployment would be higher, inflation even lower, penalising the young and indebted the most” (Financial Times, October 25). Moreover, even more banks would have gone broke and had to be rescued.

The ECB’s answer to those in major European financial powers like Britain and Germany who are running a campaign for a return to “more normal” levels of interest rates is that modest recovery is well under way and, with it, gradual restoration of bank profitability already being boosted by ECB actions (see “Recent developments in the composition and cost of bank funding in the Euro Area”, ECB Economic Bulletin No. 1, 2016 for details).

By contrast, the Swedish Riksbank’s suggestion seems to be to use the crisis of bank profitability to carry out a “shock doctrine” restructuring of the whole banking system so as to radically cut costs (just as happened after Sweden’s 1991-92 banking system meltdown), thus laying the foundations for a leap forward in competitiveness.

Are these the only options? The big assumption in the whole discussion of the low rates of return on banking in the Euro Area is that getting private bank profits back to normal “healthy” levels is an urgent and necessary task. Is it? The banking crisis and the forced “nationalisation” of crisis-hit banks like Spain’s Bankia — basically still under the control of the board that bankrupted it — point the way to a better alternative.

It is to keep banks rescued at taxpayer expense in public ownership and devote them to the work private banking does so badly: to fund investment in “green plans”, the urgently needed and job-creating renewal of infrastructure for sustainability. Such a “Green New Deal” would, by the way, also put upward pressure on low interest rates, which are at bottom due to the vast global “savings glut” frustrated of avenues of sufficiently profitable investment.

Indeed, getting the banking system to do its job properly requires, at the very least, some indifference towards bank profitability. In the Spanish state, the private banks are holding as assets hundreds of thousands of housing units left over from the 2003-2008 housing bubble that has burdened the country with three million unoccupied units. The banks are waiting for housing demand and prices to rise sufficiently before releasing them onto the market at a rate that would bring them gain. In the meantime 300,000 people go without shelter every night.

Santander, BBVA and the rest should get an ultimatum — make those empty flats and houses available for rent or purchase or face public takeover. If they reply (possibly correctly) that this would put them at risk of bankruptcy, let them follow in the footsteps of Bankia.

The end result would be, at the very least, a powerful public banking system well able to compete with the privates because it is free from the compulsion to maximise returns to shareholders. And if this approach led to the bulk of the banking system being in public ownership it would bring still further advantages such as reduction in the costs of banking system supervision, greater certainty as to the impact of monetary policy and — most important of all — rising public awareness that our society’s financial functions can be carried out perfectly well without a tribe of millionaire bankers.

{kind=link}

{kind=link}

{kind=link}

First reply to your response

Dick,

I feel surprised and honoured that you have taken considerable effort and time to reply to my comments and queries, to which I regrettably cannot respond straightaway at length, right now. You provide new and interesting data. I hope to have more time later to respond. As you indicate yourself, I was only responding to and querying a few specific points you made, not offering a complete analysis of the state of the banks. In contrast to the popular image of "evil banks", I intended to convey, that in reality banks are very constrained in what they are able to do, often much more so than ordinary business. That is also one reason for the rapid growth of shadow banking.

I can agree with many points you have stated here. Financial Times editor Martin Wolf expressed puzzlement already in 2013 about the paradox, that "the world economy has been generating more savings than businesses wish to use, even at very low interest rates." (Martin Wolf, "Why the future looks sluggish." Financial Times, 19 November 2013). Bernanke called it a "savings glut."

It is rather obvious, that if many businesses don't want to make major additional investments, then the banks will not be able to lend out the capital to them either. And if businesses don't want to invest more, there is obviously a reason for that as well: mainly, they don't think that the investment will pay itself off quickly enough, through more sales revenue, or they think that the risks are too great with an uncertain economic outlook. The rate of market expansion, of which real GDP growth is considered to be an indicator, is simply not rising fast enough for them. And at least part of the explanation for that is that real wages have stagnated; the proportion of gross profit in GDP has increased relative to the wage bill (if you factor in demographics, it's a "wage squeeze"). In Germany a while ago, bankers and politicians spectacularly called on the government for policies to raise wages!

I do not exactly know what your graph represents, but if credit provision in the EU has recovered to a level approximately the same as it was before the crash of 2008/2009, then it cannot be the case, that the aggregate demand for loans is "subdued." What I tried to say is this: there are *always* plenty people who want to get loans, the potential loan market is huge in that sense, but whether they get the loans, depends to a large extent on their credit-worthiness, their credit rating, their capacity to repay. Banks calculate their risks, costs and returns, and issue loans on that basis, or not. The reality is that, relatively speaking, there just aren't big profits in lending services to the majority of ordinary depositors and savers, the ordinary wage and salary earners. Don't take my word for it though - ask a few bankers yourself.

However, what we really need here, is a more differentiated analysis of who the lenders actually are, what sector they are in. There are loans to consumers for mortgages and durables, there are loans to producers for plant & equipment or bridging operations, but there are also loans to facilitate asset transactions. My reading of the situation is, that banks have no particular problem with issuing certain types of loans, but have heavily restricted other kinds of loans, changing the pattern of credit provision considerably.

I do not want to make specific proposals for banking reform here. It is easy to say that it is grossly unfair, that the taxpaying citizens must foot the bill if banks go bust, and suffer austerity. But you also have to remember that millions of people contracted, out of their own volition, to take out loans from banks which they now have difficulty paying back, or cannot repay. And obviously if large banks are simply left to their own devices to crash and go bankrupt, this can have very large implications for the banking system as a whole; in the worst case, it would freeze the banking system. It's easy to blame other people but - leaving aside clear cases of criminality and fraud - what we ought to be looking at, is what would work better.

Publicly owned banking makes sense for small savers and depositors, of which there are many. But nationalizing all banks (1) doesn't necessarily clear up all the accumulated problems there are, (2) has vast political repercussions, and (3) assumes that public servants would be the better judge of what good banking is about. Yet, most of the public servants do not actually know enough about banking, so then... they would be contracting in private bankers, to help them run the show. You would have banking based on political criteria, and then the banking would only be as good as the quality of the political class that governs it. If however there are already severe concerns by voters about the real competency of politicians, how good will the public banking be?