'New Politics' on 'What next in the Greek crisis?'

[The Greece-EU “agreement” has set off debates on the left on why the SYRIZA government "agreed" to such harsh terms and what are the next steps for the left in Greece, and across Europe. Links International Journal of Socialist Renewal hopes to contribute to this by providing essential background information, thoughtful comment and presenting the positions of various left organisations.]

For more on Greece's struggle against austerity, click HERE

By Barry Finger

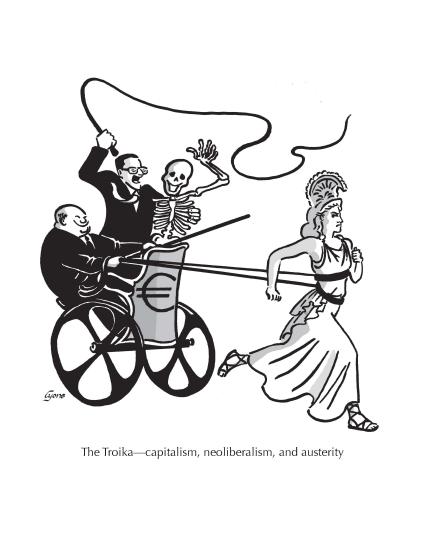

July 2015 -- New Politics (USA), posted at Links International Journal of Socialist Renewal – If the ongoing standoff between the SYRIZA government and the Troika of the European Union (EU), European Central Bank (ECB), and International Monetary Fund (IMF) could be boiled down to its essentials, it would be this: The “institutions” will only equip the Greek economy with enough operating funds to manage a bare-bones operation. And they will begrudgingly accede to this only if SYRIZA maintains a primary surplus and the neoliberal labour market reforms that the Troika judges necessary to keep the Greek economy, and other eurozone economies, competitive in the global market. The left-wing government must, in essence, demonstrate that its loyalty to the European bankers’ project takes precedence over its obligations to democracy.

If accepted, this means, for SYRIZA, that it will not be able to implement its anti-austerity measures—the massive public works projects needed to revive the country’s economy, expand its tax base, or drive down its public debt through growth. Bailout of the private and national central banks, which had or still hold sovereign Greek debt on their balance sheets, is, in any case, now being internalised by the ECB by means of quantitative easing. These toxic assets have been swapped out for euros at terms far in excess of their actual market values. This is not a complete bailout of the banking system. It will not restore that sector to its previous level of profitability. But quantitative easing is sufficient to guarantee eurozone-banking-system liquidity should the Greeks refuse to listen to “reason” and renege on their “commitments,” thereby triggering a run on the banks.

This dispute is no longer about maintaining the structural integrity of European capitalism, which has been shored up in advance, but about fashioning an unmistakable demonstration for would-be movements to challenge the status quo.

And this has already had the intended dampening effect, as evidenced by Podemos’ disappointing results in the Andalusian elections.

But national banks do not exist merely to lubricate the European economies. That ultimately is the role of the European Central Bank and, to a lesser extent, of the IMF. Private banks are primarily profit-making institutions. They make their profits on the spread between the rates at which they borrow, in the final analysis, from the ECB to maintain operating reserves, and that which can be extracted from their borrowers. Quantitative easing can be counted upon to keep bond rates low. But the banks, nevertheless, cannot find promising private entities in this profit-barren economy to lend money to, despite the rather meager profit margins the banks might be willing to accept. Industrial and commercial enterprises cannot make lucrative use of their existing capacity and so are loathe to expand. Debt-ridden workers are already under water and can, in any case, declare bankruptcy, leaving banks holding the bag.

This is not the case with nations and governments. There is no mechanism for them to write off excess debt. And, lacking a proper sovereign bank to underwrite fiscal decisions in accordance with the popular will, nations are captive to private market forces. So the bloodletting continues: austerity in exchange for loans. A housebroken Greece is to be granted future loan rollovers, arranged through the Troika, to pay off and service existing loans ad infinitum—a permanent Ponzi scheme, with no identifiable end game. And the only collateral that Greece can provide against these loans is its public assets, its cultural resources, and its tax base, all of which are rapidly shrinking in value due in no small part to the imposition of the “bailout” system itself.

In the meantime, as this is being written, SYRIZA has been forced to give its creditors, now basically the ECB, an ongoing veto over measures that might impact the economy, Greek banks, or the budget. It has to finance its state from tax receipts and cannot bridge the gap between receipts and expenditures by issuing short-term bonds to the ECB, which has already capped what it is willing to accept. The ECB has failed to lift the limits on what Greek banks can borrow under the Emergency Lending Assistance scheme. Neither has it requalified the Greek banks to borrow from the ECB. Tying off the last loose end, the ECB has, as well, prevented Greek banks from accepting government bonds needed to raise short-term capital. The Greek government and the Greek economy are gripped in an ever-tightening vise. Promised financial assistance of 7.2 billion has been held hostage since August of last year. In a variant of “your money or your life,” SYRIZA is faced with this: Contribute to the restoration of euro banking profitability and recognise your ongoing subordination to the neoliberal project, or your regime and your economy will be on indefinite lock down. Accept these conditions, and be kept on short rations.

Greek companies and households, according to the Financial Times, “pulled 7.6 [billion] out of their bank accounts during the government standoff with its international bailout creditors in February, driving deposits down to 140.5 [billion]—the lowest level in 10 years”. All this makes the need for capital controls an all but inescapable imperative.

This power asymmetry was baked into the EU framework. All nations, upon joining the eurozone, ceded their fiscal autonomy to an unelected banking technocracy. Unlike the consolidated federal banking system in, say, the United States, England, China, or Japan, the ECB exists by mandate solely to maintain price stability. It does this by setting key interest rates and by, supposedly, controlling the money supply—neither of which, incidentally, are directly meaningful in stemming state-induced inflation. And while the ECB can have a determining effect on interest rates, it cannot, in actual fact, control the money supply since all private banks create money by issuing loans. What the ECB can do, and what private banks cannot do for themselves under all circumstances, is to backstop the private banks by making available adequate operating funds to conduct business. The ECB has the sole ability to spend euros into existence. As such, the ECB, unlike private banks, can never run out of money.

The ECB’s demand that its loans be repaid is therefore a political demand and cannot be seen otherwise. It has no functional meaning beyond enforcing fiscal discipline, since “repayment” by Greece, other nations, or any other entity with which the ECB conducts business has absolutely no effect on the ECB’s ongoing ability to maintain operations. Repayment is nothing more than ledger decoration. If repayments were made in physical euros, rather than in electronic keystroke entries, the physical euros would simply be shredded.

But the ECB also has, by design, no mandate to maintain full employment. And, more generally, it has no mandate to support any of the spending decisions of democratically authorised governments. Countries that issue their own sovereign currencies, in contrast, are never revenue-constrained. Such governments are themselves the sources of the money needed to pay for their own expenditures. They are not revenue-dependent on their populations, either as sources of taxes or of loans. Taxes, under such circumstances, exist first to drive state-issued monies, by defining the medium under which government liabilities can be lawfully extinguished. They then exist as tools for siphoning off inflationary (excessive) demand, for redistribution, for carving out additional fiscal space to expand the public sector, and for discouraging activities deemed detrimental to the public welfare.

Foreign contracts, like domestic public contracts, when denominated in the national currency, can always be serviced in money the countries’ central banks have the bottomless capacity to issue. Countries that issue their own sovereign currencies cannot suffer sovereign debt crises.

It follows from this that anything that a currency-issuing economy is capable of producing, given the limits of its accumulated capacity, it also can fully afford to produce. And until the point of full capacity utilisation is reached, no nation can be justly said to be living beyond its means.

The architecture of the European Union has quite simply robbed the constituent nations of this autonomy. It has created debt colonies subject to perpetual domination at the hands of an autonomous, unshackled, central banking system. That banking system has appointed itself, by dint of prior social engineering, the executive committee of Europe’s ruling classes. And its agenda is clear. The Troika is prioritising, for the moment, rent seeking and national exploitation over jump-starting the productive sectors of capitalism until the latter is drained of its social-welfare legacy and overhead. The financial sector is enriching itself, while preparing capitalism for renewed accumulation based on a more propitious basis for exploitation and profit extraction.

Social democracy has largely surrendered to this agenda without resistance. It is only the pace and timing of implementation, rather than the agenda itself, that distinguishes its mainstream from the business community “austerians,” as SYRIZA calls them.

Once a socialist or radical left has ruled out a similar capitulation, there are really only two alternative solutions to this. On the one hand, SYRIZA can challenge the existing limits, find stopgap measures that free fiscal space, implement as much of its program as this permits, elbow the monetary union into a looser federation, and build a multinational insurgency within the eurozone having, as its intermediate aim, the socialisation of the ECB. That is, it can advocate and work for the ultimate subordination of the ECB to democratic norms and accountability by relentlessly pushing boundaries and recruiting allies within the existing framework.

Or it can prepare for as orderly an exit from the zone as it can negotiate and go it—for the moment—alone. It can repudiate its external debt or write it down and redenominate the remainder of that debt in its own newly defined currency. Greek socialists can choose, in other words, to operate on the political terrain that they have already “hegemonised” and which plays to their acquired strengths. By so doing, SYRIZA can regain Greece’s fiscal autonomy on a national basis. It can, through example, be a beacon of inspiration to other oppressed nations, who may be similarly emboldened to peel themselves away from the monetary union. With enough defections, the future of the union as a bankers’ dictatorship might itself be placed in jeopardy, precipitating a later regroupment on a different institutional footing.

But, while a Grexit (a Greek exit from the eurozone) will reclaim the essential monetary and fiscal levers the government now lacks, these levers will not overcome the structural dependence of the Greek economy on foreign investment, nor shield it from the pressures of global finance. Greek capitalism, with the exception of merchant shipping and tourism, is largely based on small enterprises. Extensive nationalisation would be difficult to coordinate, inherently chaotic, and probably politically and economically unwise. Even ardent proponents of an early Grexit, such as Marxist economist Costas Lapavitsas, restrict their calls for nationalisation to the banking sector and to those public utilities that were previously privatised. Alluding to the New Economic Policy experiment in the Soviet Union, Lapavitsas has raised the distinction between public control, which may only entail the disciplining of capital combined with extensive public works programs, and a widespread socialisation project, reserved for the remote future.

The immediate aftermath of departure would have to be meticulously planned in advance—something we have yet to see—and the population prepared for the likelihood of extensive rationing as the prices of imported goods skyrocket. This may lead SYRIZA to impose controls on the movement of capital and commodities. While the SYRIZA government, liberated from restraints from on high, should be able to mobilise the available resources to jump-start its economy, the economy it jump-starts will still be one of relative deprivation—and one vulnerable to continuous siege from the continental forces at its perimeter.

Did the Greek electorate sign up for this when they voted for SYRIZA? Are the citizens being mobilised to confront these issues? How are they being readied to face these challenges? Will the question be put to a vote? And if so, by whom? The existing government? Or a new one created to effect the transition?

What is even more worrisome than a planned and orderly exit, however, is indecision and drift. For there is certainly a yawning gap between Germany’s hysterical demonisation of SYRIZA, and SYRIZA’s actions. If, for instance, the Greek banks, unfettered by capital controls, are permitted to become insolvent in a prolonged impasse, Greece would be compelled to print its own currency under conditions not of its own choosing and under ad hoc circumstances for which it had not adequately prepared. Recourse to this contingency, under emergency settings, would signal that the decision had already been implicitly made on high that the cost of letting Greece exit the eurozone is lower than the costs of granting variances that would later have to be scaled up in answer to a euro-periphery insisting on similar deals. A “Grexident”, rather than a planned exit would add another dimension of turmoil and upheaval to an already perilous situation.

There is still another dimension to this. While the ECB retains the ability to shore up the system against liquidity shortfalls in the event of a departure, the prospect of future fragmentation is worrisome for capital on a different front. It introduces a mountain of new investor risk and uncertainty. Would Spanish, Portuguese, Irish, or Italian corporations issue bonds to raise funds in euros, if a later redenomination would cause them to go under? Would a corporation invest outside its own country if there were ongoing uncertainty about the future denomination of its investment? If a Grexit is followed by peripheral fragmentation, crises and paralysis contagion could set in, undermining neoliberal integration and leading predictably to wide-spread financial retrenchment. The Troika must be evaluating a response to this scenario. But how? By turning a blind eye to Greek initiatives that formally violate the terms of agreement, but keep Greece from exiting? Or with plans to isolate and crush an “independent” Greek economy, demonstrating decisively that the path out of the eurozone leads from disaster to ruin?

What has to be kept in mind is that there is no legal framework for Germany and the Troika to expel Greece from the Economic and Monetary Union of the EU. Greece must elect to do so freely, or be made to do so under duress. The initiative, in any case, formally resides solely with the Greeks.

The lack of a legal framework for expulsion accords SYRIZA with an unintended license for experimentation and maneuver. France and Italy, for instance, have already set precedence by missing deficit and structural adjustment targets, suffering little or no consequences for having done so. Germany violated the limits on its external balance. The Greek finance minister, Varoufakis, failed to convince the Troika to swap out existing debt instruments for perpetual interest bonds that would not add to the public debt for lack of a principal repayment obligation. Varoufakis tested the waters. But Greece’s overlords were not about to be complicit in SYRIZA’s efforts to jump-start its economy even by means that were in technical compliance with budgetary proscriptions. Clearly, an expansionary fiscal policy is something that cannot be negotiated. It is an obstacle that must be surmounted creatively, but without assistance.

One method, and one which Varoufakis evidently considered in 2013, would be for the Greek government to generate a parallel currency for internal transactions. They have already committed themselves to ramping up the intensity and efficiency of tax collection. This is probably the one place where SYRIZA and the Troika agree. When the necessary institutional changes are implemented, the Greek government can begin to securitise future taxes and issue scrip based on revenue anticipation. This scrip can be an electronic entry into accounts, personal and corporate, with which the government has business. Or it can be issued in small denomination bills intended for day-to-day purchases. It is denominated, in either case, in euros, with an exchange rate of parity. Euros will remain the unit of account, but scrip can be introduced as an additional means of payment. And since this means of payment is only acceptable for internal transactions, scrip is implicitly a form of direct capital control.

This parallel currency should be acceptable for settlement of private-sector tax liabilities and must be transferrable within the nation and to foreigners who have business or pay taxes in Greece. It is precisely a scrip’s acceptability to extinguish tax liabilities that assures its ability to circulate. It is in effect a short-term loan granted by the population to the government. And because it is perpetual without a defined maturity date requiring repayment of principal, it would not technically increase the public debt-to-GDP ratio. On the contrary, if used to prime the pump of economic expansion, it should reduce that ratio. Moreover, as long as the government makes no effort to pay principal or interest on existing government bonds, it can avoid the danger of triggering default clauses.

Because this proposed scrip would be pegged to the euro and in demand as a means of tax payment, the process of arbitrage should be sufficient to maintain par value. If its market exchange rate falls below par, taxpayers might be expected to scramble after cheap scrip to meet their obligations, which, after all, will be accepted at par value by the treasury. This process of driving up the scrip’s exchange value with the euro should be sufficient to counterbalance speculative forces operating to undermine the peg.

Socialist economist Michael Burke has pointed out that Greek business claims the highest share of national income among countries in the Organisation for Economic Cooperation and Development, at 56 per cent. Of this, only 11.3 per cent of the national income is actually invested. This is a vast pool of surplus value that can be socialised. There is no reason why this untapped remainder cannot provide a firm platform to securitise taxes for countercyclical activity. With adequate capital controls, SYRIZA is in a position to present business with a Hobson’s choice: Either invest this savings now or it will be confiscated and spent by the state later. In the meantime, these savings will be securitised as scrip for immediate relief.

Scrip can pay civil servants and support the expansion of public services. With it, SYRIZA can fund infrastructural improvements and research and development needed to earn additional euros for Greece through improved trade and import substitution. And at the same time, it frees euros for the large-scale import purchases of food, medicine, and fuel. It offers SYRIZA the opportunity to build a commanding heights to the Greek economy, which is crucial for any future socialist transformation. And it augers the possibility that Greece may no longer face the Troika as a supplicant.

But neither is this a sufficient plan B. Even if the fiscal restraint imposed by the eurozone’s limiting of primary deficits to 3 per cent of GDP were circumvented, its tax base would still restrain a Greek economic recovery. The advantages to this parallel currency is that it permits a path through which the tax base, once securitised, can pump a self-expanding loop through the system generating additional incomes to tax. Scrip issuance would allow Greece to run a fiscal deficit with at least perfunctory debt service potential until the economy recovers, and to do so without borrowing from the institutions. Any recovery would increase Greece’s credit-worthiness and SYRIZA’s bargaining strength. Nevertheless, the type of robust recovery needed is still unlikely given the country’s structural limitations. According to one estimate, Greece needs to run a primary deficit of 10 percent to return it to a fully elaborated growth path. Without the total fiscal autonomy of a supportive central bank, this is unlikely to be attained.

Can the ECB still starve SYRIZA of euros and lock up the Greek economy? There are two issues involved here. Clearly the government would no longer be dependent on receipt of additional euros to pay for public services. Euros here would have been displaced by scrip for that purpose. And again, banks create money when they issue loans. So a banking system that is again lending money would create additional system-wide reserves. But would these reserves be adequate to fully cover the additional loan exposure of a reviving economy and offset possible future bank runs, without also being backstopped by the ECB? This is where the power of the Troika resides: The ECB alone can do that. Because of fear of ECB abandonment, Greek banks are unwilling to extend short-term operating loans. This, in turn, is blocking otherwise viable Greek exporters from fulfilling their contracts and taking on new business. And that business is vital to obtaining additional euros.

How can this be offset? Beyond what can be generated by scrip, Greece, which is Germany’s seventh largest customer for military equipment, could rip up existing contracts and earmark those funds to bank reserves. It can similarly review and repudiate any other public contracts with foreign nations and firms that do not serve the commonweal. Greece is still earning euros through shipping and tourism. These euros need to be sequestered in special bank accounts and swapped out for scrip to conduct internal transactions. Investment bank accounts should not be insured by the state. And SYRIZA should fully renounce its “odious” debt obligations to further tighten centralised oversight over the leakage of euros that promise no tangible benefit to the Greek population. It can, in other words, find creative ways of economising on the use of euros while freeing itself, in the short term, from the ECB.

And there is the larger picture. What such stop-gap measures can do is to transform the eurozone from a monetary union to a looser monetary federation. Greece can “exit austerity without exiting the euro.” It can chip away at the power of the Troika and provide hope and encouragement to similarly minded insurgencies such as Podemos, Sinn Fein, and trade union militants eager to break with or move existing mass workers’ parties to the left. By stoking the anti-austerity brushfire, any success by SYRIZA, no matter how modest, would mobilise an emboldened left to ask larger questions about the structure, design, and necessity of this bankers’ federation.

This is not the time for left critics of SYRIZA abroad to pass judgment, to issue edicts from on high, or to grandstand with revolutionary rhetoric devoid of concrete substance. SYRIZA will sort this out in dialog with the Greek people. It is a time to fully comprehend the enormous obstacles SYRIZA faces in implementing its program. It is a time, above all, for constructive, comradely engagement; a time to think this through together.

[Barry Finger is an editorial board member of New Politics.]

Greek military spending

Throughout history, debt and war have been constant partners

Giles Fraser

Somewhere in a Greek jail, the former defence minister, Akis Tsochatzopoulos, watches the financial crisis unfold. I wonder how partly responsible he feels? In 2013, Akis (as he is popularly known) went down for 20 years, finally succumbing to the waves of financial scandal to which his name had long been associated. For alongside the lavish spending, the houses and the dodgy tax returns, there was bribery, and it was the €8m appreciation he received from the German arms dealer, Ferrostaal, for the Greek government’s purchase of Type 214 submarines, that sent him to prison.

There is this idea that the Greeks got themselves into this current mess because they paid themselves too much for doing too little. Well, maybe. But it’s not the complete picture. For the Greeks also got themselves into debt for the oldest reason in the book – one might even argue, for the very reason that public debt itself was first invented – to raise and support an army. The state’s need for quick money to raise an army is how industrial-scale money lending comes into business (in the face of the church’s historic opposition to usury). Indeed, in the west, one might even stretch to say that large-scale public debt began as a way to finance military intervention in the Middle East – ie the crusades. And just as rescuing Jerusalem from the Turks was the justification for massive military spending in the middle ages, so the fear of Turkey has been the reason given for recent Greek spending. Along with German subs, the Greeks have bought French frigates, US F16s and German Leopard 2 tanks. In the 1980s, for example, the Greeks spent an average of 6.2% of their GDP on defence compared with a European average of 2.9%. In the years following their EU entry, the Greeks were the world’s fourth-highest spenders on conventional weaponry.

So, to recap: corrupt German companies bribed corrupt Greek politicians to buy German weapons. And then a German chancellor presses for austerity on the Greek people to pay back the loans they took out (with Germans banks) at massive interest, for the weapons they bought off them in the first place. Is this an unfair characterisation? A bit. It wasn’t just Germany. And there were many other factors at play in the escalation of Greek debt. But the postwar difference between the Germans and the Greeks is not the tired stereotype that the former are hardworking and the latter are lazy, but rather that, among other things, the Germans have, for obvious reasons, been restricted in their military spending. And they have benefited massively from that.

The phrase “military-industrial complex” is one of those cliches of 70s leftwing radicalism, but it was Dwight D Eisenhower, a five-star general no less, who warned against its creeping power in his final speech as president. “This conjunction of an immense military establishment and a large arms industry is new in the American experience. The total influence – economic, political, even spiritual – is felt in every city, every state house, every office of the federal government … we must not fail to comprehend its grave implications. Our toil, resources and livelihood are all involved; so is the very structure of our society.” Ike was right.

This week, Church House, C of E HQ, hosted a conference sponsored by the arms dealers Lockheed Martin and MBDA Missile Systems. We preach about turning swords into ploughs yet help normalise an industry that turns them back again. The archbishop of Canterbury has been pretty solid on Wonga and trying to put legal loan sharks out of business. Now the church needs to take this up a level. For the debts that cripple entire countries come mostly from spending on war, not on pensions. And we don’t say this nearly enough.