Ukraine’s debt: An instrument of pressure and spoliation in the hands of creditors

First published at CADTM.

Ukraine’s internal and external public debt has increased by 60% between early 2022 and end of November 2024. It amounted to just under USD 100 billion before the invasion and reached almost USD 160 billion by the end of 2024, including USD 45 billion of internal public debt.1 Creditors with whom Ukraine’s debt has most increased are the European Union, the World Bank and the IMF.

Huge debt to EU

Ukraine’s debt to the EU has multiplied more than eight times. From USD 5 billion in early 2022 it rose to USD 43 billion at the end of 2024. If we add Ukraine’s debt to the European Investment Bank (EIB) and to the European Bank for Reconstruction and Development (EBRD), it reaches USD 47 billion.

This is the first point to be stressed: the EU’s financial aid comes as loans not as grants. Consequently, the EU is owed more and more, which gives it significant power over the Kyiv government. The EU’s credit policy is perverse: repayment will not start before several years. In exchange for loans, the EU demands that Ukraine adapts its legislation to the European treaties, which all favour the private sector, that it opens its procurements to private competition.

The major European private corporations are eager to reap the benefits of Ukraine’s integration into the large European market at a time when it will be in a very weak position and there will be major contracts for reconstruction to be had.

Ukraine’s other main creditors

Ukraine’s debt to the World Bank has more than tripled, rising from USD 6.2 billion to 20 billion.

Ukraine’s debt to the IMF between early 2022 and the end of November 2024 went from USD 14 to 17.6 billion. It is worth emphasizing that both the IMF and the WB continue to demand repayments, despite the war. Furthermore, the IMF practises abusive interest rates of up to 8 %. Ukraine reimbursed USD 2.4 billion to the IMF in 2022, 3.4 billion in 2023 and 3.1 billion in 2024. In other words, the IMF collected almost USD 9 billion off the back of the Ukrainians over three years of war!

The debt to the United States is nil as Washington prefers to donate rather than lend it money. Nevertheless, Washington oversees the policies of the IMF and the World Bank, and are quite able to exert any amount of pressure, should they see fit. In any case, Ukraine is so highly dependent on arms from the United States that Washington is in a position to bend the Zelensky government’s policies in any way it wishes.

The debt owed to Russia having been under suspension of payment since 2015, it has not changed and remains at USD 0.6 billion.

Ukraine’s external public debt

The debt Ukraine owes to the finance markets in the form of sovereign bonds acquired by investment funds such as BlackRock or the major banks has fallen slightly, from USD 20 billion to USD 18.2 billion. So the stock has been slightly reduced but the creditors’ position has been consolidated due to the debt payment rescheduling arranged in the second semester of 2024.

The private creditors agreed to exchange the old bonds, which had been under suspension of payment since July 2022, for new ones of less value but that would bring in juicy interest rates, higher than the previous ones. In the end, the private creditors did best from the negotiations, as before they took place, Ukrainian bonds had lost 70% of their worth. They were being sold on the secondary market at 30% of their initial value.

Since the beginning of the invasion of Ukraine in February 2022, external public debt has more than doubled, rising from USD 56 billion to 115 billion.

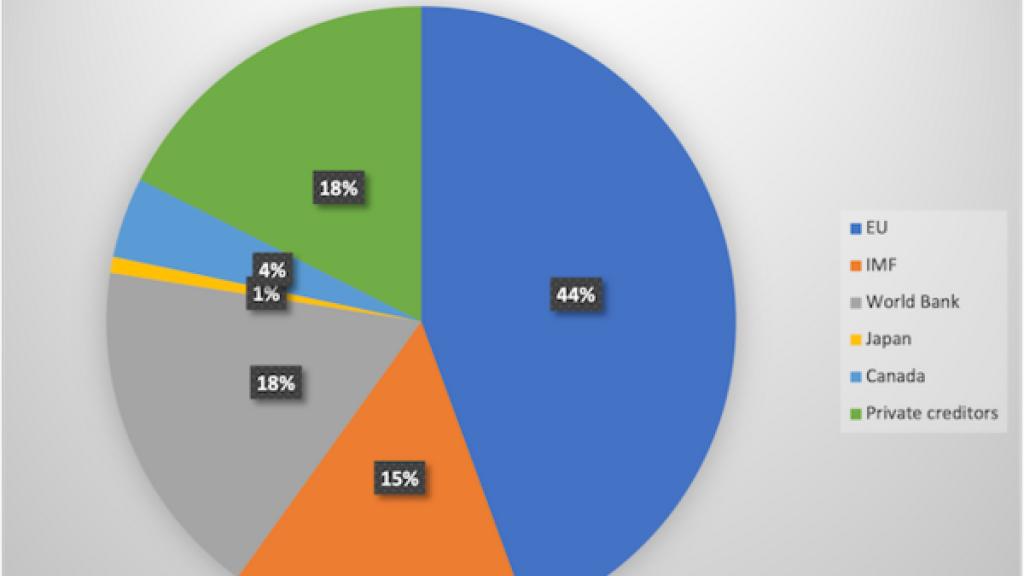

Ukraine’s external public debt which comes to a little over USD 115 billion is distributed as follows: just under USD 50 billion owed to the EU, 20 billion to the World Bank, 18 billion to the IMF, 5.2 billion to Canada, 1 billion to Japan and 20 billion US dollars owed to private creditors on the financial markets.

By percentage, 44% of Ukraine’s public external debt is owed to the EU, about 33% to the World Bank and the IMF together, 4% and 1% to Canada and Japan respectively, and about 18% to foreign private creditors (who mainly hold Ukrainian sovereign securities restructured in September 2024).

Consequences of EU, World Bank and IMF being the main creditors

In exchange for the loans granted by the EU, the IMF and the WB, the Ukrainian government accepted 325 conditionalities and recommendations.

As indicated by the Ukrainian Minister of Finance on his site, the 325 conditionalities and recommendations are grouped together in a list of reforms and measures that Ukraine is committed to implementing, in order to get financial support from international partners.2

For the creditors, it is a matter of intensifying the implementation of neoliberal policies instigated for more than 30 years.

To pursue the implementation of these conditionalities and recommendations, 531 indicators have been adopted. If Ukraine does not adhere to the calendar and the list of reforms, their partners, especially the World Bank, the IMF and the European Union, may suspend or postpone granting the loans that the country needs. These institutions keep a continuous eye on the application and the expansion of the neoliberal policies that they demand and that the neoliberal Zelensky government supports.

In 2024, the EU, the United States and other G7 members agreed on the new aid plan for Ukraine. Within this framework, the EU adopted a plan amounting to up to 50 billion euros for the period 2024 to 2027. The plan adopted provides for a total disbursement of 38.27 billion euros between now and the end of 2027. Most of this (33 billion, that is 85%) is in the form of debts that will have to be repaid. Donations only account for 5.27 billion euros, i.e. 15%.

The donations part probably corresponds to the amount seized by the European Commission on the revenue from frozen Russian assets, mainly in Brussels (see further on the share of frozen Russian assets). In the course of the year 2024, 12.4 billion was paid. And as the European Commission states in a report published in October 2024,

Most funding under the Facility will be disbursed to the State budget on fulfilment of the conditions included in the Ukraine Plan, which sets out the reform and investment agenda for the country.

The so-called “Ukrainian Plan”, which covers the period 2024–2027, is recorded in a 331-pages document. It was concocted by the European Commission. The implementation of the Plan, which contains a host of measures that the government is committed to carrying out, is under permanent surveillance. As the European Commission says,

The support is conditional upon fulfilment of requirements linked to

-* essentials such as macro-financial stability, budget oversight, and public financial management,

-* sectoral and structural reforms and investments (necessary for the EU accession).

The government had to designate a coordinator who is their interlocutor with the European Commission and who is endowed with the powers to ensure that the calendar laid out in the Plan is respected.

The authority responsible for the effective implementation of the Ukraine Plan is the National Coordinator (Coordinator). The Coordinator acts as a single point of contact for the European Commission in monitoring (…)3

The Coordinator will monitor the implementation of the Plan on a monthly basis to track the progress made. The Government will approve a procedure for monitoring the implementation of the Plan (Procedure), which will be mandatory for all authorities involved in the implementation of the Plan.4

No illusions in EU integration process

Let us recall that in the European Treaties, which are binding, there is no mention of respecting and promoting social rights. Those were hard won through social struggle within each national framework, and are not to be found in the European Treaties, which, on the contrary, prefer to encourage competitivity between the working classes of the different member countries of the Union. Within the EU, just to give two examples, the legal minimum wage is 477 euros a month (gross) in Bulgaria, whereas in Luxemburg it is 2 571 euros, i.e. 5 times higher.

The constraints imposed by the European Treaties concern the opening up of national markets to unlimited competition, public services being opened up to private initiative, liberalizing the energy market, limiting public finance deficit, the public debt/GDP ratio and so on. There are no constraints on questions of social welfare, the legal minimum wage, neither restrictions nor convergence in the fiscal domain (which enables the EU’s tax havens to take advantage of very low tax rates on profits, as is the case for example for Ireland, the Grand Duchy of Luxembourg and plenty more), no rigorous environmental constraints, no protection of the public heritage.

A great many Ukrainians have high hopes at the perspective of joining the EU, which is presented as guaranteeing improved living conditions and social rights, better wages, less corruption. All this is a great illusion, deliberately misleading people.

On the pretext of preparing European integration,5 there will be even more privatizations in Ukraine, in particular the public company that produces and distributes energy. And even more arable land will be sold to foreign agrobusiness firms.

Concerning the above warning, some left-wingers reply that the Ukrainian government is neoliberal anyhow and that even without the EU, it would attempt to implement the policies expected by the EU.

This is true enough but the agreements with the EU towards Ukraine’s integration give more leverage to those who want to strengthen neo-liberal policies. Ukraine has signed memoranda with the EU which have the force of international treaties, and as Ukraine’s creditor, the EU is in a strong position.

This position of power will further increase as new loans add to the stock of debts owed by Ukraine to the EU. If ever a left-wing government were elected, it would face those constraints that have been accepted by the previous government.

The scope for breaking with neo-liberal policies will be very limited: it will have to enter into direct conflict with the EU and contravene the treaties. It should also be remembered that all the loans granted by the IMF and the World Bank are conditional on Ukraine pursuing the (counter-) reforms necessary for its integration into the EU.

Therefore we call upon the Ukrainian and international Left not to spread any illusions about the alleged benefits of joining the EU. The Ukrainian people must be told about the risks and drawbacks that are involved. Of course they may choose to integrate the EU, but the Left has a duty to inform them about its negative consequences.

Contrary to a widespread idea among Western left-wingers, the Ukrainian economy is not at all adapted to neoliberal tenets; integrating the EU would involve lots of privatizations. The economic sector that is currently not yet privatized or subjected to free and unlimited competition is still significant.

In August 2024, the cost of repaying the public debt (50 billion hryvna, the Ukrainian currency) was almost as high as social and health expenditure.

Russian assets frozen by traditional imperialist powers

As part of the sanctions imposed since the invasion in February 2022, the G7 powers have frozen Russian assets worth around USD 300 billion. The equivalent of almost EUR 260 billion in cash and securities, such as shares and bonds, are held by Euroclear, a Brussels-based private financial institution that handles the settlement of international securities. Around USD 5 billion of Russian assets are frozen in the United States.

In 2024, the G7 decided not to expropriate Russian assets but to keep them frozen. On the basis of the Russian assets frozen in Europe, mainly in Brussels, the EU created a mechanism to issue debt securities “in favour of” Ukraine. The Russian assets serve as collateral for the large investment funds and banks that might buy securities from this loan. The money borrowed by the EU will then be paid to Ukraine mainly in the form of loans that Ukraine will have to repay to the EU.

Meanwhile the EU is getting a very good deal, repaying the financial markets for the loan (which it took out itself) with the income earned by Euroclear and others from the frozen Russian assets invested on the markets. It is estimated that the income from investments made with frozen Russian assets amounts to around EUR 5 billion a year.

Pension funds and major banks that buy securities to help Ukraine will be repaid with the income from Russian assets invested on the markets. The loan does not cost the EU a penny, while making it look generous and strengthening its position as Ukraine’s creditor as the country’s war-debt increases.

European banks in Russia

Meanwhile, several European private banks such as the Austrian Raiffaisen, the German Deutsche Bank and Commerzbank, the Italian Unicredit and Intesa Sanpaolo have not discontinued their activities in the Russian Federation. In spite of sanctions, they have multiplied their profits fourfold in that country since the beginning of the invasion of Ukraine. In March-April 2024, they paid EUR 800 million tax on profits to the Russian government without any measures being taken by EU authorities (see Financial Times revelations).

I haven’t had time to inquire further but it is striking to note that the Austrian private bank Raiffaisen that is still active in Russia in spite of sanctions is also active in Ukraine and is one of the 11 official primary dealers of the debt sold by the Ukrainian government on the financial markets (see the list of 11 banks selected to buy Ukrainian securities on the Ukrainian government’s website). Raiffaisen is thus creditor of both Russia and Ukraine and operates in Russia despite the sanctions against Russia, which it is supposed to respect.

Why support canceling Ukraine’s debt?

We have to be aware of the fact that Zelensky’s government does not wish the Ukrainian debt to be cancelled. As a good neoliberal, he is convinced that Ukraine has to be credible to private creditors.

Instead of trying to finance war and reconstruction expenses by having the rich Ukrainian capitalists, Ukrainian and foreign companies pay, he prefers to impose maximum taxation on the popular classes as recommended by the IMF and the World Bank. High incomes are spared, the assets of the richest remain untouched. Thus the rich, who manage to evade enrolment in the army, can heap up wealth while the popular classes make huge sacrifices.

Another method used by the Zelensky government to finance its budget is to contract loans. It borrows on the internal market, notably from oligarchs’ banks and from the very rich who bought internal public debt securities in 2024 at rates of up to 16.5%.6 The inflation rate in 2024 was around 10-11%. The Central Bank’s key rate was 13.5%.

The debts Ukraine had accumulated before the Russian invasion in February 2022 were both illegitimate and odious since the borrowed money had been used to carry out neocolonial policies that were clearly opposed to the interests of the population. Moreover, they had favoured the massive enrichment of a privileged minority through grabbing formerly public goods. Creditors, i.e. mainly the IMF, the WB, the oligarchs and investment funds, were well aware that the loans they granted would not serve the general interest.

As we have seen, since the beginning of the war the EU has become the main creditor as it has multiplied its loans to Ukraine by 8, while the WB’s loans have been multiplied by 3 and the IMF has also increased its loans. Those creditors use their credits to impose reinforced neoliberal policies on the population. Ukraine’s newly accumulated debts are thus also illegitimate and odious.

It is important to get them cancelled /repudiated so that the creditors are deprived of the leverage they have at their disposal and to prevent them from enriching themselves on the backs of the Ukrainian people. If Ukraine and its people want to regain their sovereignty, they must free themselves from the yoke of the creditors who are acting in their own interests and against those of the Ukrainian people.

Resistance to the Russian invasion and reconstruction efforts could be financed in other ways than through debts: through grants, on one hand, and through taxing the war profiteers, on the other.

Other measures

Concerning the financing of Ukraine’s resistance and reconstruction, I mentioned the following proposals besides debt cancellation in an article published in May 2024: the assets of both Russian and Ukrainian oligarchs who profit from the war should be seized. Significant amounts could thus be collected to finance the Ukrainian people’s resistance and the country’s reconstruction.

Let us note that if a tax were levied equivalent to the additional profits made by arms companies in the context of this war and other wars in general, this would limit the propensity of these companies to rejoice in the continuation of the war and to contribute to it, since they would not benefit directly from it.

Measures to seize oligarchs’ assets, and confiscate and expropriate their property, run directly counter to the sanctity of private property. As a result, there have been no major seizures since 2022 because Western governments are not inclined to do so, even if they oppose the Russian Federation.

Exactly what has been accomplished needs to be assessed, but in any case, it has been extremely limited and nothing has been transferred to any fund controlled by the Ukrainian people. In fact, there has been no specific tax on corporations that have benefited from the war.

I mentioned the arms companies, but we can also discuss the massive profits made by gas and oil companies as a result of Russia’s invasion of Ukraine. Profits have also increased for grain marketing corporations around the world, including the four big multinationals that control 80% of the global cereal grains trade. They include three US companies and one European company. A special tax on the profits of these companies should have been levied and should be levied, including retroactively, both to finance the needs of all populations and to help the Ukrainian people.

We must also continue to demand the cancellation of Ukraine’s debt.

We could add the socialization of the banking sector. As indicated above, about half of the banking sector is still public but not truly in the service of the population, which would involve measures such as transparency of accounts, citizens’ control, monitoring of local elected representatives, decentralization. The private part of the banking sector ought to be expropriated and socialized to establish a monopoly of the public banking sector (except for small-size cooperatives if they are truly controlled by their members).

The state still has a monopoly on the energy sector. Contrary to what is expected by the EU, the WB and the IMF, this monopoly must be maintained and democratized. Citizens and workers in this sector must be able to control accounts, prices and management. In short, the energy sector too must be socialized.

The state should develop the construction of small-size electricity production units managed by local communities, much easier to protect, secure and manage. This also involves much less wastage during transportation to consumers. New small production units should not use fossil energies. We also need to prepare for an accelerated phase-out of nuclear power and to give up fossil fuels.

To be able to move towards a form of peace and reconstruction in the service of populations, it is essential to develop all possible forms of self-organization.

The author is grateful to Antoine Larrache, Maxime Perriot and Patrick Saurin for their comments. Translated by Christine Pagnoulle and Vicki Briault Manus, CADTM. Eric Toussaint is a historian and political scientist who completed his Ph.D. at the universities of Paris VIII and Liège. He is also the spokesperson of CADTM International and sits on the Scientific Council of ATTAC France.

- 1

Data from Ukraine’s finance Ministry: https://mof.gov.ua/en/derzhavnij-borg-ta-garantovanij-derzhavju-borg

- 2

“A list of commitments for implementing reforms that Ukraine has undertaken to receive financial support from international partners.” https://reformmatrix.mof.gov.ua/en/index/ accessed on 16/1/2025.

- 3

“The authority responsible for the effective implementation of the Ukraine Plan is the National Coordinator (Coordinator). The Coordinator acts as a single point of contact for the European Commission in monitoring,” p. 314. On the Ukrainian government’s website, https://www.ukrainefacility.me.gov.ua/en/ On the European Union’s website, https://neighbourhood-enlargement.ec.europa.eu/document/download/1924a044-b30f-48a2-99c1-50edeac14da1_en?filename=Ukraine%20Report%202024.pdf, accessed on 6/1/2025.

- 4

p. 316. Op. cit., accessed on 16/1/2025.

- 5

In a European Commission report dated 30 October 2024, we read, “Ukraine applied for EU membership on 28 February 2022, and was granted European perspective and candidate country status in June 2022. In December 2023, the European Council decided to open negotiations with Ukraine. The first inter-governmental conference opening the negotiations took place on 25 June 2024”. Source: https://neighbourhood-enlargement.ec.europa.eu/document/download/1924a044-b30f-48a2-99c1-50edeac14da1_en?filename=Ukraine%20Report%202024.pdf accessed on 16 January 2025.

- 6

See the website of Ukraine’s national Bank https://bank.gov.ua/en/news/all/u-2024-rotsi-uryad-zaluchiv-vid-prodaju-ovdp-na-auktsionah-mayje-640-mlrd-grn-v-ekvivalenti-a-zagalom-uprodovj-voyennogo-stanu--mayje-1-458-mlrd-grn-v-ekvivalenti A lot of information can be found there on public securities of the internal debt that is issued in the national currency, in dollars and in euros. An Excel sheet mentions all issuances of war securities: Purchase of military domestic government debt securities between 24 February 2022 and 31 December 2024. See also https://mof.gov.ua/en/borgova-politika accessed on 16 January 2025.