European financial system: next crash just around the corner?

ECB financing operations

The situation would have been even worse had it not been for the European Central Bank’s longer-term refinancing operations (LTRO), begun in late 2011. The LTRO handed banks hundreds of billions at one per cent interest, which they often invested in government bonds at higher interest rates. This was money for jam that helped banks reduce their own indebtedness, at the expense of government budgets in which debt servicing payments became an ever larger line item.

Next, in mid-2012, came the ECB’s decision to undertake Outright Monetary Transactions (OMT) — the purchasing of government debt in secondary markets — in order to help drive down interest rate on public debt in the “periphery”, in fulfilment of ECB governor Mario Draghi’s undertaking to do “whatever it takes” to save the euro.

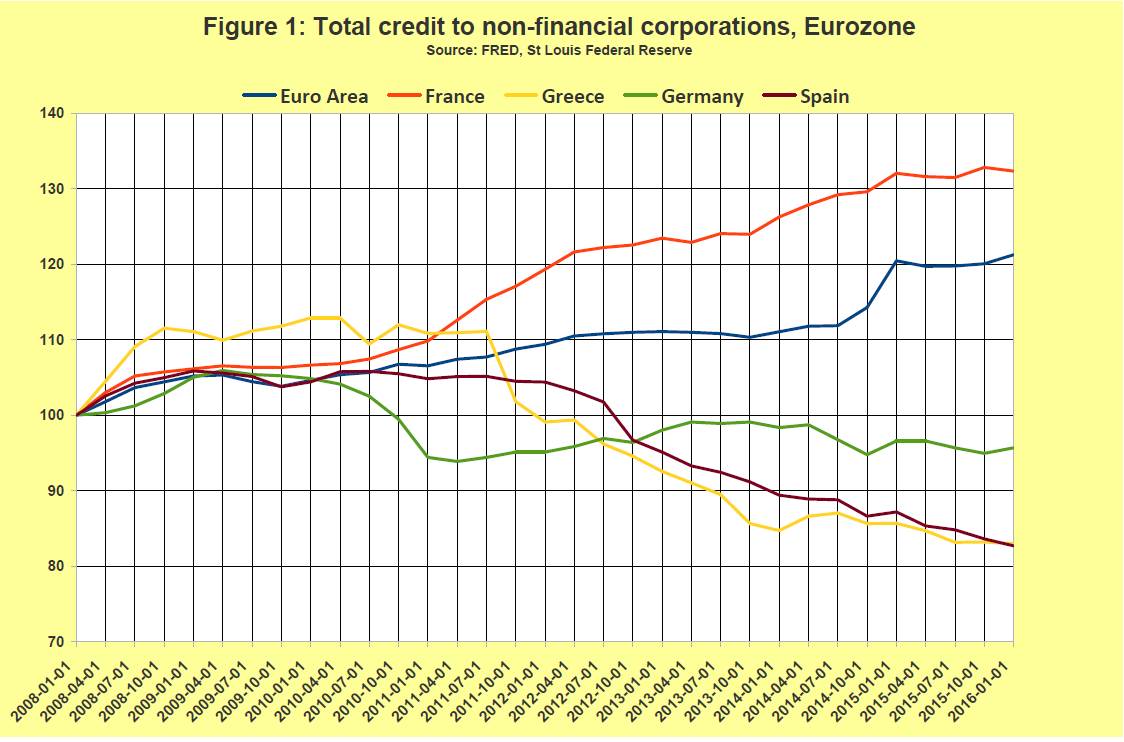

Finally, by the beginning of 2014, there was a mild pick-up in bank lending to business that was reinforced by the ECB’s next initiative — targeted longer-term refinancing operations (TLTRO). This was a program to effectively give banks money on condition that these funds were used to finance credit to small and medium business and not to speculate on the bond market or real estate (a major destination of LTRO funds).

However, by the end of 2015 the TLTRO was also running out of steam, with banks increasingly not taking up the ECB’s very generous offer because demand for credit was simply not there. A second phase of TLTRO began in June.

It is doubtful how much take-up there will be of TLTRO II. In the words of one anonymous finance commentator cited on the Zero Hedge web site: “The lack of positive real expected returns dampens new investments in hiring plans, plant and machinery, and related borrowing and credit formation with it. Thus, [ECB president Mario] Draghi’s move was just another artefact of financial leverage, not a game changer.”

The result of the ECB’s expansionary monetary operations, conventional and unconventional, has been to underpin what very mild growth there has been in the Eurozone since 2013, but at the very high cost of producing overvalued and increasingly volatile financial markets (especially share and bond markets), as the beneficiaries of ECB largesse hunt for some return in the world of low and negative interest rates driven by stagnating rates of investment and growth.

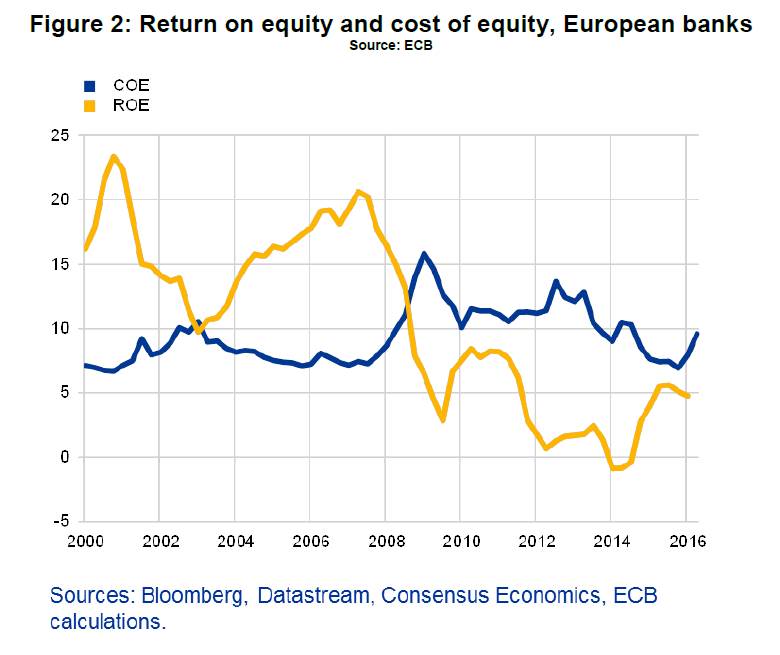

For the banking sector the end result of the operation of all these tendencies is chronically low profitability (see Figure 2). In the euro area average bank return on equity (income after costs as a ratio of shareholder equity) was at 5.8% in early 2016. This is not only less than the 10% generally accepted in the industry as a “good performance number”, it was less than the cost of capital (cost of raising funds via equity and/or loans and estimated at around 9%). Chronic instability

The low profitability of banking is set to continue because it is driven by three very intractable factors: the huge stock of non-performing loans; the low, even negative, interest rate environment caused by the low demand for credit; and the ongoing overcapacity in an industry that it also being challenged by developments in new financial technology (“fintech”) such as crowd-funding, peer-to-peer lending and private money systems like Bitcoin.

In this context even national banking sectors that have carried out “successful” reconstructions (such as Spain, where bank branches have been reduced from 45,000 to 30,000 and staff by one-third), safety is fleeting, as the fragile situation of Banco Popular reveals. Bad news about a troubled financial institution can readily send it on the road to ruin if twitchy investors and depositors fear that their bank is in danger of failing and start to pull their money out, producing the very annihilating bank run they fear.

This is the brink on which both Deutsche Bank and Monte dei Paschi di Siena are now perched: they are at the point where paper thin confidence in their future could give way before any more bad news, producing the “rush for the exits” that finished off Lehman Brothers in 2008.

If Monte dei Paschi failed it could probably be incorporated into some other Italian bank, just as Bear Stearns and other failing banks were snapped for a song by J. P. Morgan Chase in 2008. However, a Deutsche Bank failure would be qualitatively more destructive because of the sheer size of the banks obligations to other major banks, including central banks, and the range of its trading activities (especially in derivatives).

The latest news from Deutsche Bank is that it lost 5% of its total deposits and 13% of its demand deposits in the July-September quarter — suggesting the possible start of a bank run. If this is the case, intervention from the German government of Angela Merkel must loom on the horizon. The German chancellor has said that the government has no intention of intervening to help the bank, but this is an institution that really is too big—and too connected with the rest of the European and global financial system — to be allowed to go under.

On October 27, Deutsche Bank reported its third quarter result, revealing its biggest profit in more than a year at €278 million (compared to a €6 billion loss in the same quarter last year). Did this mean that, after all the panic, Deutsche Bank had turned the corner?

The share market did not think so: the bank’s shares continued to slide because it still needs to carry out a massive restructuring to regain profitability. The present profit figure represented a miserable two per cent return on equity, and this in a quarter that was good for banks worldwide. Moreover, although revenues rose three per cent to €7.5b billion, the bank’s asset management fund shrank by €8 billion and its liquidity reserves fell by 10 % to €200 billion.

And the politics?

It is not excluded that Monte dei Paschi, Deutsche Bank (and others) will survive in some shape or other. But whatever the result, the political price for the financial and political establishment will be very big.

In the case of outright bank failures, who will pay for cleaning up the mess? If it is the taxpayer (via bail-out) — as with the €53 billion restructuring of the Spanish financial system — some version of the indignado response of “rescue people, not banks” is certain. If it is the depositors (via “bail-in”), protest might be contained in the exceptional case that the operation is like that of Cyprus’s March 2013 bank restructuring: there the majority of those forced to take a “hair-cut” on their deposits were Russian émigrés and other overseas investors.

More likely, the reaction will be like that in Italy in late 2015, when the government forced the bondholders of four small banks to take losses. There were extensive protests, one pensioner who lost his investment of €100,000 committed suicide, and the populist Five Star movement got a big boost that contributed to its later winning important mayoralties, including that of Rome, in June this year.

And if bank restructuring, by some miracle, gets carried out by the “natural” processes of takeover, branch closures and job destruction? In Spain, even though the protests of the tens of thousands of finance sector workers threatened with job loss in the banks that survived the crisis have not stopped restructuring, their anger has had real political impact: it has both deepened popular rejection of the financial elite and the politicians at their beck and call and made the need for a different banking system a matter of broad public debate.

All of which is already having increasingly strong feedback effects on the stability of the financial world itself — even on those institution apparently far from Deutsche Bank’s and Monte dei Paschi’s predicament. In the October 14 Financial Times, correspondent Gillian Tett wrote: “[T]he real danger in finance is not one that tends to be discussed: that banks will topple over (as they did in 2008). It is, rather, the threat that investors and investment groups will be wiped out by wild price swings from an unexpected political shock, be that central bank policy swings, trade bans, election results or Brexit.”

If the present state of siege in the European banking sector has emerged at the peak of a phase of anaemic growth, what will a future of slowing growth and even recession hold for it?

Dick Nichols is the European correspondent of Green Left Weekly. An initial version of this article has already appeared on its web site.

Chronic instability

The low profitability of banking is set to continue because it is driven by three very intractable factors: the huge stock of non-performing loans; the low, even negative, interest rate environment caused by the low demand for credit; and the ongoing overcapacity in an industry that it also being challenged by developments in new financial technology (“fintech”) such as crowd-funding, peer-to-peer lending and private money systems like Bitcoin.

In this context even national banking sectors that have carried out “successful” reconstructions (such as Spain, where bank branches have been reduced from 45,000 to 30,000 and staff by one-third), safety is fleeting, as the fragile situation of Banco Popular reveals. Bad news about a troubled financial institution can readily send it on the road to ruin if twitchy investors and depositors fear that their bank is in danger of failing and start to pull their money out, producing the very annihilating bank run they fear.

This is the brink on which both Deutsche Bank and Monte dei Paschi di Siena are now perched: they are at the point where paper thin confidence in their future could give way before any more bad news, producing the “rush for the exits” that finished off Lehman Brothers in 2008.

If Monte dei Paschi failed it could probably be incorporated into some other Italian bank, just as Bear Stearns and other failing banks were snapped for a song by J. P. Morgan Chase in 2008. However, a Deutsche Bank failure would be qualitatively more destructive because of the sheer size of the banks obligations to other major banks, including central banks, and the range of its trading activities (especially in derivatives).

The latest news from Deutsche Bank is that it lost 5% of its total deposits and 13% of its demand deposits in the July-September quarter — suggesting the possible start of a bank run. If this is the case, intervention from the German government of Angela Merkel must loom on the horizon. The German chancellor has said that the government has no intention of intervening to help the bank, but this is an institution that really is too big—and too connected with the rest of the European and global financial system — to be allowed to go under.

On October 27, Deutsche Bank reported its third quarter result, revealing its biggest profit in more than a year at €278 million (compared to a €6 billion loss in the same quarter last year). Did this mean that, after all the panic, Deutsche Bank had turned the corner?

The share market did not think so: the bank’s shares continued to slide because it still needs to carry out a massive restructuring to regain profitability. The present profit figure represented a miserable two per cent return on equity, and this in a quarter that was good for banks worldwide. Moreover, although revenues rose three per cent to €7.5b billion, the bank’s asset management fund shrank by €8 billion and its liquidity reserves fell by 10 % to €200 billion.

And the politics?

It is not excluded that Monte dei Paschi, Deutsche Bank (and others) will survive in some shape or other. But whatever the result, the political price for the financial and political establishment will be very big.

In the case of outright bank failures, who will pay for cleaning up the mess? If it is the taxpayer (via bail-out) — as with the €53 billion restructuring of the Spanish financial system — some version of the indignado response of “rescue people, not banks” is certain. If it is the depositors (via “bail-in”), protest might be contained in the exceptional case that the operation is like that of Cyprus’s March 2013 bank restructuring: there the majority of those forced to take a “hair-cut” on their deposits were Russian émigrés and other overseas investors.

More likely, the reaction will be like that in Italy in late 2015, when the government forced the bondholders of four small banks to take losses. There were extensive protests, one pensioner who lost his investment of €100,000 committed suicide, and the populist Five Star movement got a big boost that contributed to its later winning important mayoralties, including that of Rome, in June this year.

And if bank restructuring, by some miracle, gets carried out by the “natural” processes of takeover, branch closures and job destruction? In Spain, even though the protests of the tens of thousands of finance sector workers threatened with job loss in the banks that survived the crisis have not stopped restructuring, their anger has had real political impact: it has both deepened popular rejection of the financial elite and the politicians at their beck and call and made the need for a different banking system a matter of broad public debate.

All of which is already having increasingly strong feedback effects on the stability of the financial world itself — even on those institution apparently far from Deutsche Bank’s and Monte dei Paschi’s predicament. In the October 14 Financial Times, correspondent Gillian Tett wrote: “[T]he real danger in finance is not one that tends to be discussed: that banks will topple over (as they did in 2008). It is, rather, the threat that investors and investment groups will be wiped out by wild price swings from an unexpected political shock, be that central bank policy swings, trade bans, election results or Brexit.”

If the present state of siege in the European banking sector has emerged at the peak of a phase of anaemic growth, what will a future of slowing growth and even recession hold for it?

Dick Nichols is the European correspondent of Green Left Weekly. An initial version of this article has already appeared on its web site.

| Attachment | Size |

|---|---|

| Picture1.jpg | 111.41 KB |

| Picture2.jpg | 46.74 KB |

{kind=link}

{kind=link}

Credit markets

According to Dick Nichols, "the chief pressure squeezing bank profitability has come directly from real economic conditions, from the subdued demand for loans."

I doubt very much is that is true.

It is not really that there is a "subdued demand for loans", but that banks have been "under pressure to curb their lending". The "chief pressure" is simply that interest rates are low.

At low interest rates, the bank profit margin on bank loans is rather small, and it would take only a relatively small percentage of non-performing loans, to ensure that the bank makes no money from the loan business at all. That being the case, the risk criteria which banks use for the issuing of loans to consumers and business have been tightened up a lot.

Furthermore, most governments have imposed higher capital adequacy requirements and bank charge ceilings on banks, plus much stricter statutory loan qualifications on borrowers, which mostly have to do with the borrowers' ability to repay. For every credit operation, banks now have higher administration costs and more legal requirements as well.

All of that has the effect that it becomes much more difficult to get a loan, if you want one. The business sector which is most affected by this predicament is that of small and medium-sized business, since large corporations can usually issue their own debt. Yet it it the small and medium-sized business sector which proportionally provides most of the paid jobs.

In response to the lacklustre lending-business, banks themselves typically seek to buy assets up and businesses which they think will appreciate greatly in value. As regards securities, however, the margins are hardly spectacular in most cases, and the state typically restricts the ability of banks to make speculative investments. Ultimately therefore, it is still the real profitability of ordinary business establishments which strongly determines the overall, longterm outcomes for aggregate economic activity.

What Gillian Tett is really alluding to, is that even well-protected and secure investors have become very conservative, in a situation where relatively small fluctuations in key economic indicators can have huge financial consequences and destabilize whole countries. Trillions of dollars are now invested at a negative return in real terms, even.

For that very reason though, it becomes more likely that extra-economic (socio-political) events could touch off the kind of financial panic that causes a new slump. Even if there is no disturbance or panic though, the incremental effect of debt growth which is much faster than GDP growth is to increase socio-economic inequality and social tensions, and increase the financial vulnerability of societies.

Is this assessment valid?

Is this assessment valid? Are any independent economists leaning towards it as well?

Response by Dick Nichols

See Dick's response here http://links.org.au/europe-banking-crisis